Flexi Hoses: The $80,000 Apartment Claim Almost Everyone Could Prevent

What this guide covers

- Burst flexible braided hoses cause approximately one in five Australian water damage claims, with average claim values now exceeding $27,500.

- In nearly every Australian jurisdiction, the flexi hoses inside a lot are the lot owner's responsibility, not the body corporate's. This is widely misunderstood.

- Strata insurance covers sudden and accidental damage. Hoses that show visible wear and tear may produce reduced or declined claims.

- A committee-level maintenance program (including pressure-limiting valves, isolation taps, and bi-annual visual checks) is the most cost-effective insurance premium intervention available to most buildings.

- Why the cost of one owner's neglected flexi hose ends up on the whole building's premium.

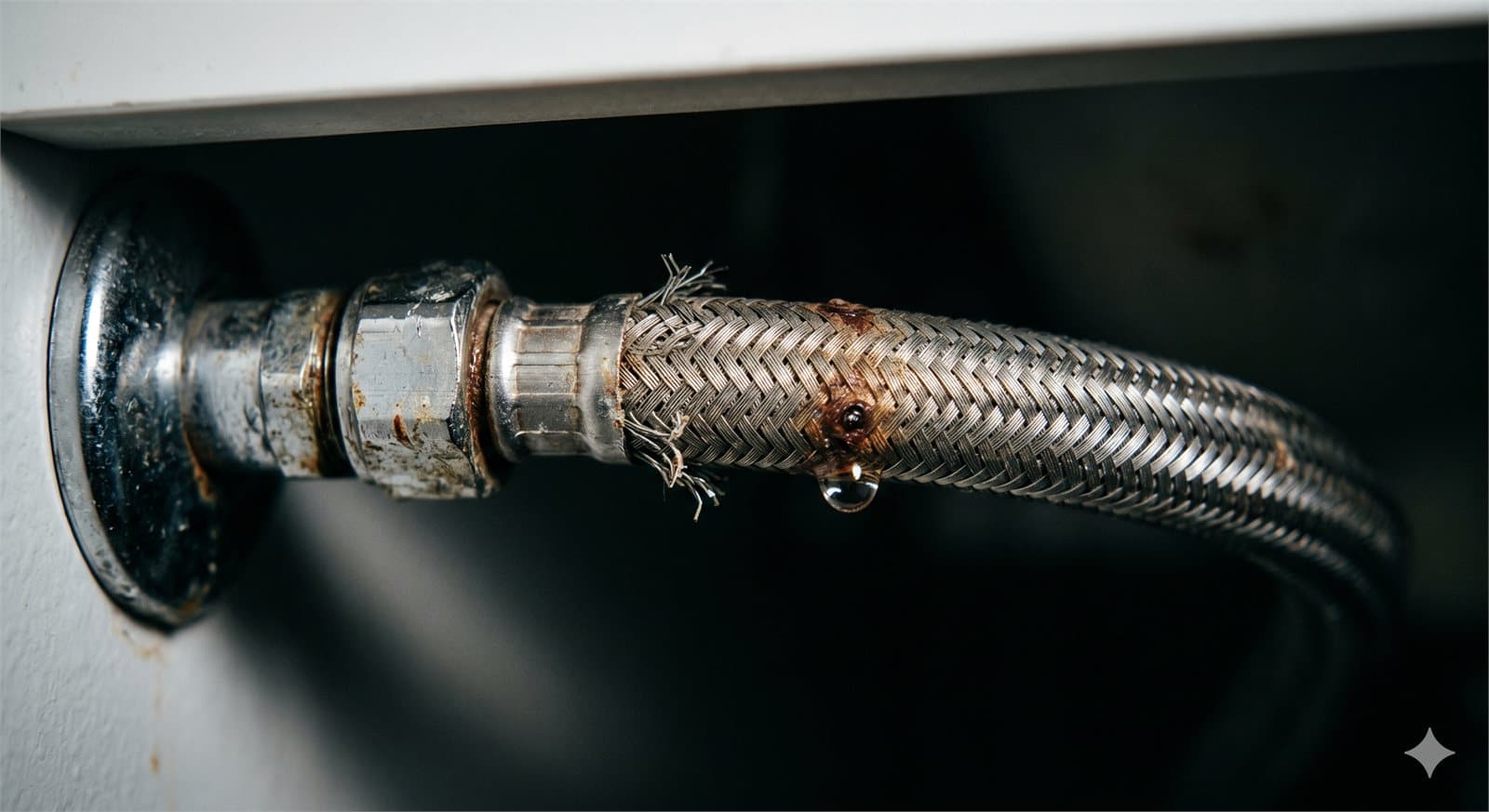

There is one piece of plumbing in nearly every Australian apartment that costs about eight dollars, lasts up to ten years, and is responsible for an outsized share of the claims pushing strata insurance premiums up. It is the flexible braided hose: the metallic-looking tube that connects taps, toilets, dishwashers, washing machines, and bathroom vanities to the water supply.

Insurers have been writing about flexi hoses for over a decade. The pattern is well documented. The hose ages quietly, the braided steel sleeve corrodes from rust or chemical exposure, the inner rubber tube fatigues from repeated pressurisation cycles, and at some point, often when the apartment is empty, the hose splits. A failed hose can release several hundred litres an hour. The water finds floors, wall cavities, electrical fittings, and the apartment below.

The economics are unforgiving. The hose itself is cheap. The damage downstream is not.

The numbers

A few representative figures from public insurer data and case studies.

Approximately 20 to 24 per cent of Australian household water damage claims are attributable to burst flexible hoses, depending on the source. CHU Underwriting Agencies has reported that more than 45 per cent of its strata water damage claims involve flexible hose failure. Strata Community Insurance has reported paying out more than $50 million in water damage claims over a recent three-year period, with flexi hoses a significant contributor.

Average claim values have risen with construction costs. QBE's 2021 figures put the average household water leak claim at around $5,000. More recent insurer data places the average per-event cost at over $27,500 in apartment settings, where damage spreads through multiple lots.

Worked examples from public case studies:

- A flexi hose in an upper-floor bathroom split while occupants were away. Water spread through three floors of a complex. Building repair bill: $80,000. Five lots uninhabitable for around four weeks. Alternative accommodation costs $350 to $500 per unit per week.

- A burst ensuite hose in a Brisbane scheme produced an $11,000 insurance excess against the body corporate's policy.

- A laundry hose failure in an unoccupied investor-owned lot ran for several hours before discovery. Reserves set by the insurer: approximately $15,000 for resultant damage repairs.

The pattern across cases is consistent: cheap component, expensive consequence, slow detection, multi-lot impact.

Why flexi hoses fail

Several reasons, all of them well understood by the plumbing trade.

Age. Flexi hoses have a manufacturer-stated lifespan that is typically five to ten years. Some come with a warranty period stamped on the collar, which is the most reliable indicator of when the hose was certified to operate. Hoses installed before 2011 may pre-date the introduction of certification standards in Australia and should be treated as end-of-life regardless of apparent condition.

Pressure cycling. Each time water flows through the hose, the inner rubber tube expands; when flow stops, it contracts. Repeated cycling fatigues the rubber. Buildings with high mains pressure see faster wear than those with lower pressure. This is why pressure-limiting valves at the building mains are one of the most cost-effective interventions a body corporate can make: they extend hose life across every lot in the building.

Heat. Hot water hoses fail faster than cold water hoses. The same fatigue mechanism, accelerated by temperature.

Installation defects. A surprisingly high proportion of failures trace back to incorrect installation rather than aged components. Common defects include over-tightening at the connections, twisting the hose during installation, kinking, stretching the hose taut between fittings, and contact with chemicals stored under sinks. Each of these reduces effective lifespan substantially. A correctly installed quality hose will typically reach its rated lifespan; an incorrectly installed hose may fail in two to three years.

Chemical exposure. Cleaning products, drain cleaners, and other corrosive substances stored under sinks can degrade the steel braiding from outside and the rubber tube from condensation effects. Bathroom and kitchen vanity storage habits matter more than most owners realise.

No maintenance program. Flexi hoses are out of sight in most installations. They are rarely inspected unless the owner deliberately looks. By the time visible signs of failure appear (rust spots, fraying, kinking, bulges) the hose is well into its failure window.

The lot vs common property question

This is the part of the picture that owners and committees most often get wrong.

Flexi hoses are connected to the internal plumbing fixtures of a lot: taps, toilets, dishwashers, washing machines. These fixtures sit inside the lot. The hoses are part of the lot's internal plumbing, not the building's common property water supply infrastructure.

In nearly every Australian jurisdiction, the responsibility position is:

- The water supply pipe up to the isolation valve at the lot is common property and is the body corporate / owners corporation responsibility.

- The plumbing inside the lot, downstream of the isolation valve (including the flexi hose) is the lot owner's responsibility to maintain and replace.

This means the lot owner pays for hose replacement and is responsible for the consequences of failure. Strata insurance may cover the resultant water damage, depending on circumstances, but the maintenance obligation sits with the owner.

Two practical corollaries.

The body corporate cannot make a rule requiring hose replacement. It can only encourage owners to replace at intervals through information and education.

A lot owner who fails to maintain a flexi hose may bear personal liability for resultant damage to other lots and common property. Strata insurance often covers this, but not always, and rarely without consequences for the building's claims record.

The commercial logic of this position is that the body corporate has no practical access to inspect inside lots regularly. Maintenance has to be the lot owner's job.

The pragmatic logic of this position breaks down when you look at insurance pricing. A claim caused by one lot's failed hose increases the premium for the whole building. The body corporate's economic interest is in reducing claims regardless of where the underlying responsibility sits, which is why the better committees run building-wide hose replacement programs even though they have no power to compel participation.

The insurance sting

Strata insurance is designed to cover sudden and accidental damage. The phrase carries weight.

A hose that bursts without warning, with no prior signs of degradation, is a sudden and accidental event. The insurer pays.

A hose that has been visibly rusting for two years, has a fraying steel braid, has been in place for fifteen years past its warranty, and finally splits, is wear and tear. Wear and tear is excluded from most strata policies. The insurer can reduce or decline the claim.

The line between "sudden" and "wear and tear" is contested in many cases. Plumbers and insurance assessors look at:

- Visible pre-failure indicators (rust, fraying, kinking, bulging, age markers on the collar).

- Plumbing reports or maintenance records prior to failure.

- The history of similar failures at the same property.

- The age of the hose at the point of failure.

Multiple prior claims at the same property change the picture significantly. If a building has had two or three prior flexi hose failures, an insurer may declare future hose-related water damage uninsured on the basis that the body corporate had constructive knowledge of the risk and failed to act.

The Australian Financial Complaints Authority has ruled on six-figure disputes arising from exactly this scenario. Owners assume the strata policy will pay; the policy excludes wear and tear; the dispute escalates; the eventual outcome is partial payment or refusal.

What a committee-level maintenance program looks like

This is the response that produces the best return on investment. A committee that takes flexi hose risk seriously can materially reduce its building's claim history within two to three years. The components:

Pressure-limiting valves at the mains. A pressure-limiting valve installed at the building's main water inlet reduces the pressure entering every lot's plumbing. This extends the operational life of every flexi hose, every fitting, and every joint in the building. Installation is a one-off cost, typically a few thousand dollars depending on building size. The economic return is several years of reduced wear across hundreds of failure points.

If your building has high mains pressure, this is the single highest-value intervention available. Ask your plumber to test the static pressure at the mains. If it is above 500 kPa, a pressure-limiting valve is almost certainly justified.

Building-wide hose replacement program under s158 (or state equivalent). The mechanism described in the Queensland smoke alarm post, where the body corporate procures collectively, lot owners opt in, and each is invoiced for their portion, works equally well for flexi hoses.

A 30-lot building can typically replace every flexi hose for $200 to $400 per lot under a coordinated procurement. The same work done by 30 individual plumbers separately would run $400 to $700 per lot. The savings come from a single contractor, scheduled efficiently, working through the building over a few days.

This is voluntary; lot owners opt in. Most do once the cost differential is explained, particularly if the body corporate frames the program as a collective insurance-premium reduction effort.

Bi-annual visual inspection program. Encourage owners (or coordinate building-wide) visual inspections every six months for signs of failure. The diagnostic indicators are visible to the naked eye:

- Rust spots on the steel braid, particularly at the collar and along bends.

- Fraying of the braided steel sheath.

- Kinks or twists in the hose.

- Bulges or swelling in the rubber inner tube where the braid has weakened.

- Discolouration of the rubber tube where visible.

- Audible signs (hissing, gurgling, unusual sounds when water flows).

A hose with any of these indicators should be replaced immediately. The replacement cost ($8 to $20 for the hose, $80 to $200 for installation) is dramatically lower than the consequences of a failure.

Resident education on isolation taps. Every lot should have an internal isolation valve allowing water supply to be shut off at the lot. Every resident should know where it is. The five seconds it takes to turn off the isolation tap when a hose fails is the difference between a $5,000 claim and a $50,000 one.

The body corporate's main valve location should also be publicly displayed somewhere accessible: the lift lobby, the laundry, the noticeboard. After-hours emergencies are common; the contractor or strata manager response time is lengthy. A neighbour who knows where the main valve is can isolate the building before significant damage spreads.

Vacant property protocols. When a lot is unoccupied for more than a few days (investor lots between tenants, owners on holiday) the water supply at the lot's isolation valve should be turned off. This eliminates the risk of an undetected hose failure running for hours. Communicate this protocol to lot owners in writing.

What an individual owner should do

For owners who want to manage this individually rather than through a building-wide program:

Check every flexi hose in your apartment annually. Look at the collar for the warranty date. If the hose is past its warranty period, replace it immediately. If it is approaching the warranty period (within a year), schedule replacement in the next quarter.

Replace hoses with a quality product. The cheapest hoses at the hardware store are not usually a good choice for components that hold pressurised water in a top-floor apartment. Spend the extra five to ten dollars on a hose with a longer warranty and certified compliance markings.

Use a licensed plumber for installation. The combination of correct tightening, correct alignment, and verification that the connections are leak-free reduces the early-failure rate substantially. The cost difference between a DIY installation and a professional one is small relative to the consequences of getting it wrong.

Avoid storing chemicals (drain cleaners, oven cleaners, bleach) in the same cupboard as a flexi hose connection. The fumes accelerate corrosion of the braided sheath.

When you go away, isolate the water supply at the lot's isolation valve. Run a tap briefly afterwards to depressurise the line. If a hose fails while you are away, the consequences will be limited to whatever water is in the building's pipes between your isolation valve and the next downstream fixture.

If your apartment shows water stains on walls or ceilings near a wet area, do not assume it is condensation or aesthetic. Investigate. Hose failures often produce slow, intermittent leaks before they produce a catastrophic burst. The slow leaks are also expensive: they produce mould, structural damage, and eventually claims that the insurer may treat as wear and tear.

Why this is everyone's problem

A common reaction from lot owners is that flexi hose risk is the body corporate's responsibility because strata insurance pays the claim. This reaction is wrong on both counts.

The hose itself is the lot owner's responsibility to maintain. The body corporate has no obligation to replace it.

The claim, if it is paid, is paid by the building's strata insurance, but the cost of the claim flows back into the building's claims history, and the building's claims history is the single largest input to the next renewal's premium. A building with three flexi hose claims in five years will see materially higher premiums than a similar building with none.

That premium increase is paid by every lot owner through levies. The economic incidence of one owner's neglected hose is shared across the whole building. This is why the most engaged committees run building-wide programs even though they cannot compel participation.

The strata insurance premiums guide covers the broader picture of why premiums have risen so much over the past five years. Claims history is one of three or four major drivers; flexi hose claims are within the building's control to reduce.

How UnitBuddy fits

UnitBuddy holds the building's maintenance calendar and contractor records. For a committee running a flexi hose replacement program, the platform supports tracking which lots have opted in, which have notified independent replacement, and which still need follow-up. The compliance and risk module surfaces the building's claims history alongside the maintenance program, so a committee can demonstrate the link between the two when negotiating the next insurance renewal.

The pressure-limiting valve installation, the s158 procurement records, and the bi-annual inspection schedule all sit in the same place. The next time an insurance broker asks what the body corporate is doing to manage water damage risk, the answer is a documented program rather than a verbal assurance.

This is methodology supported by tooling. The component that fails is a flexible braided hose. The component that prevents the failure cascade is an organised maintenance program. The latter is what UnitBuddy is built to support.

Further reading: Water Leaks From Above covers what to do when the leak comes from a neighbouring lot. Why Strata Insurance Premiums Have Skyrocketed covers the broader premium picture and the levers a committee has. Contents vs. Strata Insurance covers what each policy actually pays for when a hose fails. What Strata Insurance Actually Covers covers the wear-and-tear exclusion and how it operates in practice.